Overview

2023 saw a trend towards an omnichannel and multi-platform landscape with increased industry competition driven by traditional e-commerce platforms working to defend their existing market share against emerging platforms.

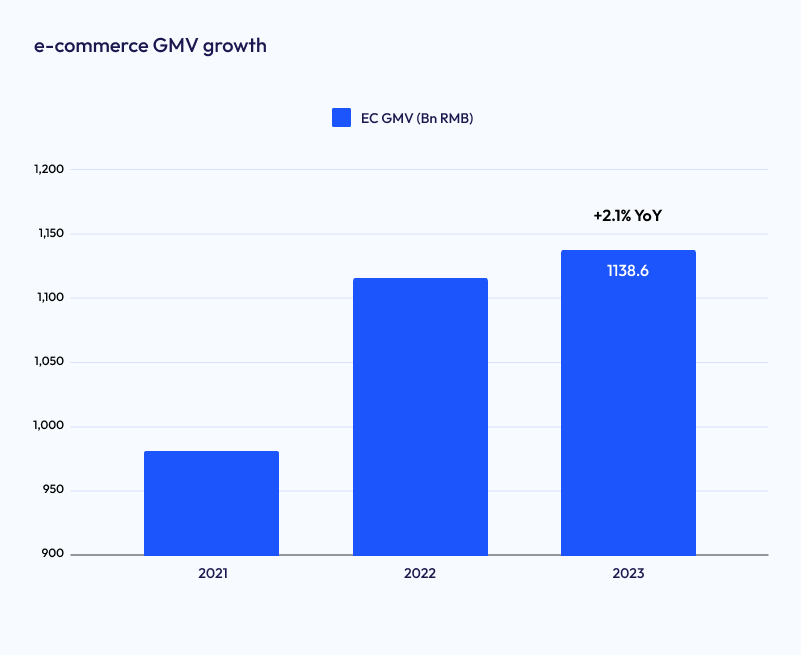

Traditional e-commerce platforms remained dominant with a total GMV of 923Bn RMB (126Bn USD), despite a 1.1% decrease across the top 3 retailers (Tmall, JD, PDD). However, emerging platforms focused on live-streaming, like Douyin, Kuaishou, and TaobaoLive, are developing rapidly with GMV reaching 215Bn RMB(29Bn USD), up to 18.6% YoY growth. Additionally, new retail platforms like Meituan Shangou, JD Delivery to Home, and Eleme, increased by 8.3% year-on-year, with an overall GMV of 24Bn RMB(3.3Bn USD).

Key Trends

Low prices are the top marketplace priority this D11

After 15 years, D11 returned to a “low price” themed event, with platforms heavily investing in

low price strategies, platform rules simplification, and a series of merchant support and preferential traffic.

Cost-effective domestic brands are exploding in popularity

With a focus on “low prices”, D11 saw local brands capture 11 of the top 20 brands (by sales) across the event. Of local brands, the most advantageous categories included: agricultural specialties (e.g. hairy crabs), skincare products, apparel and home furnishings.

A surge of "dopamine economy"

“More and more consumers, especially young consumers value the emotions that products can bring to them. They’d like to pay for happiness,” noted Aowen, President of the Brand Business Development Center of Taotian Group. This was evident with the virality of the “dopamine economy” with spikes for categories like gaming, cycling, skiing and more.

Traditionally male-dominated categories reigned supreme this D11

Reflected across Tmall, JD and other large e-commerce platforms, alcohol, digital products, gaming-related, cycling-related, Lego, designer toys, male skincare products, male perfume were popular categories this D11.

The emergence of more niche categories

Many categories that don’t typically see much growth over D11 began to gain significant traction in 2023 including intelligence products, new energy vehicles, pets, outdoor activities, and camping.

Marketplace Growth Trends

Tmall(Alibaba)

Key takeaway: Driven by user-first and AI-driven strategies, Taobao and Tmall achieved comprehensive growth across user size, merchant scale, order volume, and total GMV. This helped realize the climax of purchasers in the public and private domains, and the explosion of price power and memberships.

User-first strategies were reflected in the supply of diverse products, segmented and differentiated consumer operations, improved logistics and after-sales service experience, and better prices. Additionally AI-driven strategies were embodied directly within the platform providing tools to help merchants better calibrate pricing, apply tools to reach consumers, and spend budget to gain more traffic and consumers.

Brand business boom

402 brands (including 243 local brands) had GMV that exceeded 100M RMB

38K brands saw transactions increase by over 100%

Record-breaking user size

The cumulative number of users in this year's D11 exceeded 800M, breaking the historical record

The amount of 88 VIP exceeded 32M, also hitting a new record high, and contributing transactions saw double-digit annual growth

Enthusiastic merchants

Weekly active merchants increased 150%

Average daily number of paid advertisers increased by double-digits year-over-year

Distinct low price shopping mindset

More than 20M buyers and 140M orders in cities below the third tie

699% increase in transactions with the support of the 10 billion subsidy program

386% increase in number of buyers

More efforts in private-domain operation

100M+ users joined brands' loyalty programs

Orders made by members have increased by over 100% for several consecutive days

The harvest year of store livestream

58 livestream rooms saw GMV exceed 100M RMB, of which 38 were held by brands while 451 store livestream rooms saw GMV exceed 10M RMB

JD

Key takeaway: JD heavily focused on low price strategies and quality service over D11 this year, leading to record highs across GMV, order volume, and user size.

JD Procurement and Sales Manager Livestreaming goes viral

The total number of viewers exceeded 380M, resulting in the largest incremental growth for brands and merchants

More than 60 brands saw sales exceed 1 billion RMB

Turnover of nearly 20,000 brands increased by more than 3x

5x new merchants' GMV

More low-priced products delivered to consumers

400K+ physical stores participated in JD's D11 campaign

During D11, users of JD's “x-hour delivery” increased by 60%, and users of "delivery and installation within x-hours” increased by 80% compared to the previous month

Ochama, JD's European omni-channel retail brand

The door-to-door delivery service increased flexible fulfillment and delivery services with expansion into 24 countries across Europe, and extended business hours

Industrial AI capabilities to guarantee low prices

JD Cloud’s user visits per second increased by 170%

JD Cloud's intelligent customer service was used over 1.4M times

A series of platform support for merchants

Newly registered stores increased 3.4x, while stores participating in D11 increased 1.5x year-over-year

77% increase in number of merchants served by JD Shangzhi, JD's one-stop operation data platform, resulting in saved operation costs of over 1.2Bn RMB in total

Extra support for local brands

JD formally initiated the China Chic program, covering apparel, sports, bags and suitcases, beauty, and other categories

JD supermarket announced an investment of over 1Bn RMB to support local brands

PDD(Parent company of TEMU)

Key takeaway: PDD offered over 10 billion subsidies to its 620M users during D11, becoming the most cost-effective platform for smart phones, electronics, and home appliances.

Category growth in the first three days of D11

Pet brands saw sales volume increase by 600%

Furniture, home furnishings, new energy automobile parts and other commodities increased by more than 320%

Seafood, mutton, fruit, sports, beauty, small household appliances, electric cars, learning machines, tea and beverages, imported snacks, computer hardware, and high-end musical instruments increased by more than 110%

Users across tier one, four and five saw significant growth

The number of orders made by the first-tier cities’ users increased 113% while the value of orders made by consumers from tier four or five cities increased by 167%

Focus on local brands

On September 22nd, PDD launched a livestream featuring local brands to help boost their business growth

Douyin(Bytedance)

Key takeaway: Douyin focused on boosting brand awareness during D11 with an emphasis on shelf e-commerce and operation of Douyin Mall, search, shopping windows, and other channels.

Douyin saw record growth their 3rd year participating in D11

Shelf e-commerce led to a 156% year-on-year increase in average daily sales

Product exposure increased 1.6x that of the first half of the year

86% increase in participating merchants

Livestream EC totaled 38.21M hours, and the sales of 7,667 livestream rooms exceeded 1M RMB

Douyin Mall made record figures in its first year in D11

Drove overall merchant GMV growth of 145%, and key brands GMV growth of 244% on October 31st

Women Apparel merchants experienced robust growth

26 brands saw GMV exceed 100M RMB, with 159 stores having exceeded sales with 10M RMB, and nearly 1K products, contributing to a GMV over 1M RMB

Search and shelf scenarios harvest, with GMV improving by 78.1% and 97.8% respectively, compared to last year

Kuaishou

Key takeaway: Kuaishou focused on low prices to help convert users to purchase big-brand products. Over 100M users and 1M merchants and influencers participated in Kuaishou's D11, resulting in 50% increase in order volume, and the GMV of SMBs increased by more than 75% year-on-year.

Brands grew significantly over D11

Brand GMV grew by more than 155% year-over-year

Nearly 2,500 brands saw year-over-year growth of 100%

Brands in the consumer electronics and home furnishings categories grew by 624% year-over-year, with GMV increasing by 1,386%

Introduction of “authenticity insurance”

Aimed to encourage users to purchase products with high unit prices such as consumer electronics and household appliances

Offered subsidies for the most popular commodities such as digital and electrical appliances at different times of the day

Cooperation with JD Logistics: Kuaishou invited JD to be an official logistics partner to provide solid logistics service for its merchants and users during this year's D11

RED (Little Red Book or Xiaohongshu)

Key takeaways: RED honed in on buyer-style e-commerce, with a focus on users that had a passion for new items, lifestyle preferences, and high spending power.

RED came with the "gene" of seeding given its high quality users, with up to 200M MAU, of which up to 72% were young users. Merchants who comprehensively adopted product notes, buyer livestream, store livestream, and other forms of full-chain operations continued to emerge, becoming one of RED's key highlights during this D11.

Overall growth of RED

3.8x order volume

3.3x number of purchasers

4.1x number of participating merchants

Live-streaming was a new field for steady business growth

Store livestreaming GMV grew 6.9x

8x the number of merchants that started live-streaming

Buyers' livestream exploded at an exponential rate, with livestream GMV 3.5x year-over-year

GMV brought by RED notes was 3.6x last year, with brands like Little Austin, and MY.ORGANICS exceeding GMV of 1M+ RMB

Final Thoughts

Overall, many of D11’s e-commerce platforms (both traditional and emerging) saw exponential and often record-breaking growth during this year’s event. Many focused heavily on user experiences to drive increased conversions and sales with tactics like low prices, authenticity insurance, and more.

Ready to grow your business?

Let's discuss the best approach to meet your brand's specific needs.

Let's connect